As 2023 comes to an end, we find ourselves contemplating a year filled with valuable lessons, joyous moments, and formidable challenges. This past year, being the inaugural complete cycle of Pulpan Brothers Group at Christie's International Real Estate Sereno, has been particularly noteworthy. Among the myriad lessons learned, a standout realization has been the profound, although often unnoticed, influence of our everyday routines beyond the confines of the workplace on how we approach and tackle the challenges presented within. Looking ahead to 2024, my aspiration is to create a more well rounded daily routine and adhere to its consistent implementation.

The subject matters I would like to discuss are as follows:

-

Interest Rates

-

Supply Levels

-

Securing Insurance in 2024

-

Bank Term Lending Program

-

Grateful for You

Interest Rates

The Federal Reserve's final meeting of 2023 concluded with a decision to maintain the target rate at 5.25% - 5.50%. Jerome Powell's notable shift in tone hinted at 3 rate cuts in 2024, diverging from the earlier stance of "higher for longer." Despite four rate hikes in 2023, Powell expressed flexibility in adjusting rates based on inflation progress. The two-sided risks involve insufficient suppression of rising costs or waiting too long to cut, leading to a recession with increased unemployment and falling GDP.

Recent economic indicators include Headline CPI at 3.1%, below expectations, driven by lower energy costs. Unemployment decreased to 3.7% in November, but historical patterns suggest it may peak after the first rate cut, a potential concern for 2024. Powell shared during the meeting, "We... anticipate continued progress on inflation, but the path likely will be bumpy, and the risks are two-sided... we will maintain flexibility to adjust the pace of adjustments in the federal funds rate as appropriate."

Markets interpreted Powell's message as signaling earlier rate cuts, with a current 50%+ chance of the first cut in March 2024. The expectation aligns with a historical trend mentioned in our previous newsletter, anticipating rate cuts 9 months after the "pause" (July 2023). Despite this, I think we will see our first cut during the middle portion of next year.

Current mortgage rates range from high to mid-6’s, a decrease of 1.5% since mid-October. Anticipated mortgage rates for early to mid-2024 are expected to stay in the mid to low 6% range with the possibility of seeing sub 6% by the end of the year.

Supply Levels

As we approached the close of 2022, we asserted that while mortgage rates dominated headlines, the true bottleneck in 2023 would be the limited housing supply. The initial half of 2023 witnessed a staggering 40% year-over-year decrease in inventory for single-family homes in Santa Clara County. Inventory did improve nominally as the year progressed but was also met with the return of seasonal constraints.

|

New Listing /Mo |

2022 |

2023 |

Delta ∆ |

|

October |

677 |

718 |

6.06% |

|

November |

516 |

557 |

7.95% |

|

December |

270 |

344 |

27.4% |

*MLS data provided | Single Family Homes | Santa Clara County

This severe strain on supply prompted a swift rebound in the median sales price, reaching its lowest point in December 2022. To provide context, the pinnacle of the market was observed in Q2 2022, marked by a median sales price of $1,950,000 for single-family homes across Santa Clara County. By September 2023, prices reached their yearly peak at $1,840,000, reflecting a 5.6% overall decline despite the concurrent increase in borrowing costs. While prices have subsequently undergone seasonal adjustments, they still stand 16% higher than their December 2022 levels.

|

Median Sales Price ($) |

2022 |

2023 |

Delta ∆ |

|

October |

$1,586,500 |

$1,800,000 |

13.46% |

|

November |

$1,572,500 |

$1,680,000 |

6.84% |

|

December |

$1,465,000 |

$1,700,000 |

16.04% |

*MLS data provided | Single Family Homes | Santa Clara County

Looking ahead to the coming year, we anticipate an enhancement in current supply levels. Two primary factors will drive this improvement. Firstly, the diminishing trend in mortgage rates will re-engage more "step-up" sellers in the marketplace. The past year predominantly saw life event sales, such as those related to death, divorce, retirement, etc as those with fixed sub 4% mortgage rates refused to exchange their current home for one with 7% financing. Secondly, the Baby Boomer demographic progressing into retirement age, will contribute to an increase in supply. By the year 2030, all Baby Boomers will be at least 65 years old. However, despite the influence of these factors, it will take a few years before we witness pre-COVID inventory levels in Santa Clara County.

|

New Listing/Yr |

Units |

|

2018 |

12,964 |

|

2019 |

11,892 |

|

2020 |

12,086 |

|

2021 |

13,461 |

|

2022 |

11,291 |

|

2023 |

8,600 |

*MLS data provided | Single Family Homes | Santa Clara County

Securing Insurance in 2024

California has witnessed the destruction of nearly 10 million acres of forest and 39,000 homes due to wildfires in the past five years, underscoring the severity of the state's forestry crisis. As a result, a concerning trend has emerged – numerous insurance carriers are opting to cease coverage for homes in specific regions or are exiting the home insurance market entirely.

Below are a few noteworthy headlines from the past year regarding insurance.

- Safeco, one of the more common policy providers in recent years, to drop policies in the Bay Area (8/4/2023). Safeco Insurance announced they were dropping 950 policies in San Francisco and the East Bay.

- Farmers Insurance limits new home insurance policies (7/10/2023). Farmers Insurance announced that it was placing a cap on new policies in California.

- Allstate no longer selling new policies (6/4/2023). Allstate, California's fourth-largest home insurer, announced they were no longer writing new policies in the state, though they will continue to renew existing policies.

- State Farm no longer selling new policies (5/31/2023). State Farm, California's largest home insurance provider, announced it would stop writing new policies. State Farm said they will continue to issue renewals to their existing customers.

- Court rules in favor of expanding the commonly perceived “last resort,” California FAIR Plan (11/29/2023). The CA FAIR Plan may soon offer more comprehensive homeowners insurance, removing the need for a DIC wraparound policy. This would now allow FAIR Plan policies to cover theft, water damage, liability, and more.

California experienced record-breaking wildfire losses, with insurers paying $15.4 billion in 2017 and $13.6 billion in 2018, significantly surpassing previous years' annual losses that never exceeded $5 billion. This led to a concerning trend of insurers paying $1.85 in losses for every $1.00 of premium earned over two consecutive years. In response, the California Department of Insurance approved 71 rate increase requests from 50 different companies in 2019, resulting in steep premium hikes for most homeowners in an effort to help insurers recover from the financial strain caused by these unprecedented wildfire seasons.

The crisis peaked in 2019 when over 230,000 policies were not renewed by insurance companies, a 42% increase from 2018. Simultaneously, new policies under the California FAIR Plan, a state-mandated last-resort option for homeowners struggling to find private market coverage, surged by 219%. Responding to the spike in nonrenewals and FAIR Plan policies, the California Department of Insurance imposed 25 moratoriums since 2019, preventing insurers from canceling or not renewing policies in wildfire-prone areas for up to one year (PolyGenius “California’s home insurance crisis”).

However, these moratoriums did not address a significant challenge: Proposition 103. This 1988 law in California adds complexity to the process of recouping losses and maintaining profitability. Home insurance companies often seek rate increases through the state's insurance department, but Prop. 103 requires insurers to justify these increases based on average annual wildfire losses over the last 20 years. Given the exponential rise in wildfire losses, insurers face the dilemma of taking on more risk than they can compensate for in premiums. The dwindling number of rate increase approvals since 2020 suggests that many insurers may have reached the limit imposed by Prop. 103, prompting them to either withdraw from certain areas or exit the state altogether.

When looking to purchase a home, please make sure to consult with your agent. They should be able to connect you with a number of brokers who can find you an optimal coverage at the best possible rate. This should be done before a noncontingent offer is submitted as you do not want to be caught off guard by these rising rates.

If you own a home, please note that construction costs have risen 34% since 2020 which has left a great deal of homeowners underinsured. Take the time to review your policy and make sure you have adequate coverage in the event of a disaster.

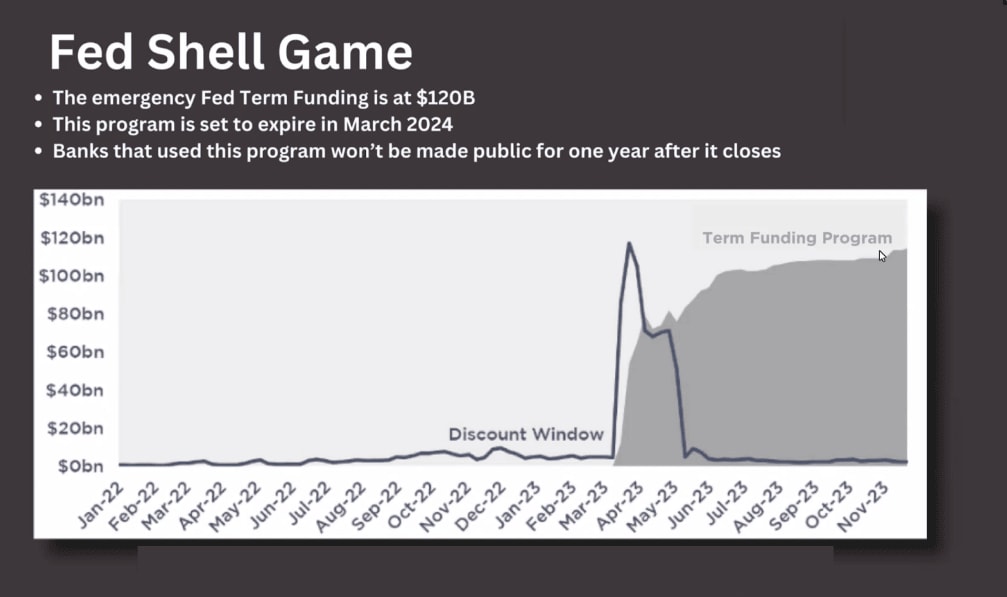

Bank Term Lending Program

The Bank Term Funding Program (BTFP) was introduced by the Federal Reserve in March 2023 as an emergency measure in response to the sudden failures of Signature Bank, First Republic Bank and Silicon Valley Bank, triggered by bank runs and rising interest rates affecting safe investments like U.S. Treasury securities. The program aims to provide liquidity to U.S. depository institutions by offering loans of up to one year to eligible borrowers, including banks, credit unions, and savings associations, using collateral such as U.S. Treasuries. The BTFP is set to wind down on March 11, 2024, unless renewed by the Federal Reserve. The initiative is distinct from the Primary Credit Lending program and involves no fees for participation. The U.S. Department of the Treasury provides credit protection, and the program's rate is updated daily and publicly available. Overall, the BTFP serves as a temporary response to banking crises, intending to support depositors and ensure the liquidity of eligible institutions.

So as the year comes to a close, where are we with the BTFB?

The intention of this program was for the banks that needed liquidity to pay the money back within the 12 month period. However, 9 months later the balance continues to grow, exceeding 130 Billion dollars in December. I am not qualified to stipulate how this is resolved or the implications on the banking sector moving forward. However, for all the headlines to claim the banking sector has returned to stabilization feels intellectually dishonest. The banks participating in this program are concealed but are unlikely to be the big banks, rather the regional, localized, smaller banks. The same banks that hold a large share of commercial real estate debt. Is it a coincidence that the markets are factoring in the first rate cut in March, the same month the BTFB is set to expire? Are rate cuts essential in providing any relief to this program? Will we see more regional bank collapses in 2024?

This is something I will be watching closely next year, in addition to household credit card debt levels which exceeded $1 trillion earlier this year.

Grateful for You

As noted earlier, in this inaugural full year of Pulpan Brothers Group at Christie's International Real Estate Sereno, I'd like to take this moment to express my deep appreciation for everyone who has entrusted us with their real estate aspirations. Establishing autonomy amidst one of the more challenging markets in recent years, the past few months have filled us with immense joy and anticipation for what lies ahead.

Our commitment is to sustain a superior level of service, ensuring our clients are well-informed at every stage of the process. We aim to provide high level insights into current market conditions and the potential risks, fostering a sense of confidence and understanding in the decisions you make.

Cheers to 2024!